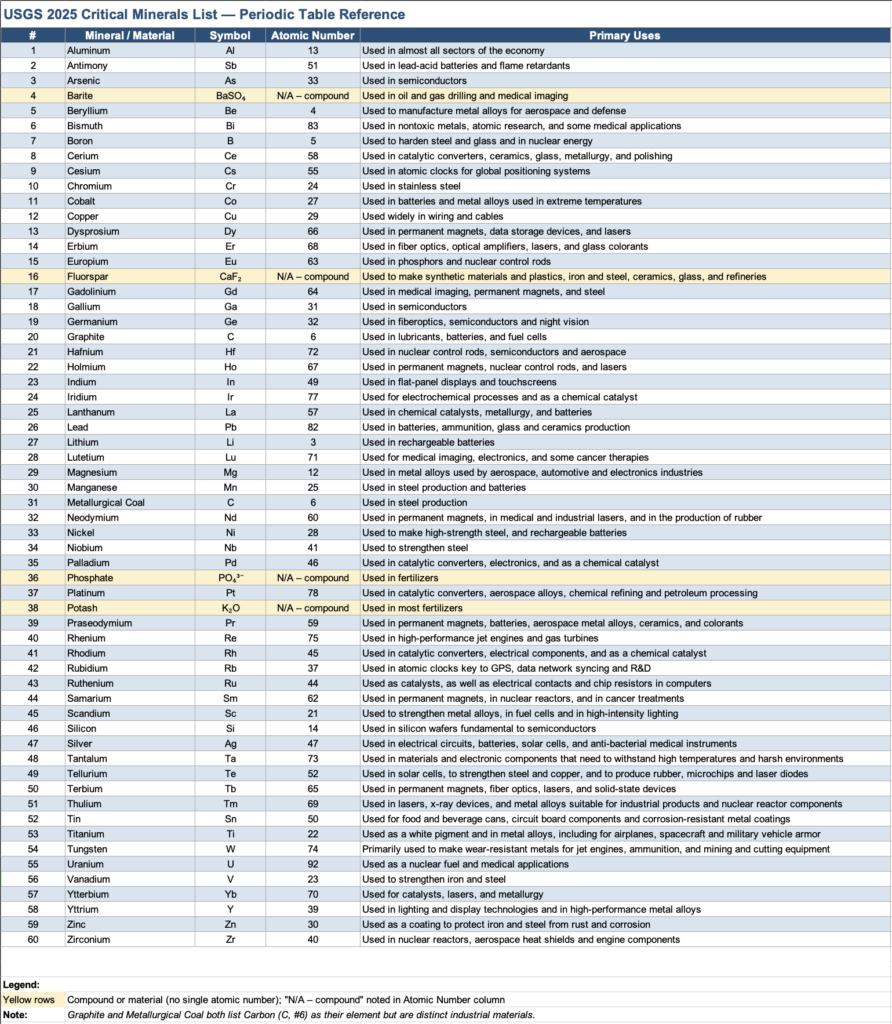

The USGS used probability-weighted GDP loss modeling across 1,200+ trade disruption scenarios to derive this ranking. The top 10 mineral commodities, in descending order by estimated probability-weighted impact of supply disruptions on the U.S. economy, are samarium, rhodium, lutetium, terbium, dysprosium, gallium, germanium, gadolinium, tungsten, and niobium. USGS

Beyond that top 10, the remaining minerals are grouped here by USGS risk tier, drawing on the same modeling framework.

TIER 1 — Highest Risk (Top 10 by GDP Impact, USGS Official Ranking)

| Rank | Mineral | Key Risk Factor |

| 1 | Samarium | ~100% China-dependent; no domestic alternative; GDP impact ~$4.5B |

| 2 | Rhodium | South Africa–dominant; $64B single-scenario GDP hit |

| 3 | Lutetium | Heavy rare earth; 80%+ China-sourced and processed |

| 4 | Terbium | China near-monopoly; critical for EV motors and defense |

| 5 | Dysprosium | China near-monopoly; essential for high-performance magnets |

| 6 | Gallium | China already used export controls in 2025; semiconductor-critical |

| 7 | Germanium | China imposed export restrictions in 2025; fiber optics and night vision |

| 8 | Gadolinium | Heavy rare earth; China-dominated supply chain |

| 9 | Tungsten | Tungsten shows a relatively smaller economic impact but a higher probability of disruption, placing it firmly in the top-risk tier. The Fuse |

| 10 | Niobium | Brazil near-monopoly; huge GDP impact if disrupted |

🟠 TIER 2 — Elevated Risk

Several additional mineral commodities including magnesium metal, potash, and rare earth elements yttrium, ytterbium, neodymium, praseodymium, europium, holmium, erbium, and thulium were also determined to have high risk. This tier also includes: USGS

- Magnesium — China produces ~85% of global supply

- Manganese — South Africa and Gabon dominant; critical for batteries and steel

- Cobalt — DRC-dominant (70%+); essential for EV batteries

- Graphite — China controls ~90% of processing; battery anodes

- Indium — China-dominant; 100% U.S. import reliance for flat panels

- Tantalum — DRC and Rwanda dominant; single-point-of-failure risk

- Neodymium / Praseodymium — Chinese rare earths; permanent magnets

- Yttrium / Ytterbium / Europium / Holmium / Erbium / Thulium / Lanthanum / Cerium — All heavily China-dependent rare earths

TIER 3 — Moderate Risk

- Platinum / Palladium / Iridium / Ruthenium / Rhenium / Rhodium — South Africa and Russia dominant; geopolitically exposed

- Lithium — Chile/Argentina/Australia dominant but diversifying; high strategic demand

- Nickel — Indonesia and Russia dominant; battery supply chains under stress

- Chromium — South Africa and Kazakhstan dominant; stainless steel

- Vanadium — China and Russia dominant; steel and battery storage

- Tin — China and Indonesia dominant; circuit boards

- Tellurium — Byproduct of copper smelting; very limited global sources

- Cesium / Rubidium / Scandium — Retained on qualitative grounds due to insufficient data

- Hafnium / Zirconium — Single domestic point-of-failure risk

- Bismuth — China-dominant; limited substitutes

- Beryllium — Single U.S. processor; domestic SPOF

- Titanium — Processing concentrated in Russia, Japan, China

TIER 4 — Lower Relative Risk (But Still Critical)

These minerals are critical but have more diversified supply chains, greater domestic production, or more available substitutes:

- Aluminum — Canada is primary supplier; relatively stable relationship

- Copper — Chile dominant but widely traded; newly added to list in 2025

- Silicon — Newly added; import reliance manageable

- Potash — ~90% from Canada; stable but large volume dependency

- Silver — Mexico dominant; newly added

- Lead — Newly added; recycling reduces primary supply risk

- Phosphate — Morocco dominant; food security concern

- Zinc — Globally distributed production

- Barite — China-dominant but substitutable in some uses

- Fluorspar — China and Mexico dominant

- Boron — Turkey dominant; added via public comment

- Uranium — Added by executive order; domestic production declining

- Metallurgical Coal — Added by executive order; domestic production exists

- Antimony — China dominant; recently targeted by export controls

- Arsenic — Re-added for national security by DoD

- Manganese — Critical but some domestic processing